Our experts analyze new innovation trends related to new financial services.

Technologies that facilitate the monetary revolution

When we talk about the technologies that facilitate the monetary revolution, the first thing is to talk about the platforms that make it possible: DLTs (Distributed Ledger Technologies) and in particular Blockchain. Blockchain platforms are distributed platforms that allow the exchange of value between their participants without the need for trusted third parties.

On Blockchain, Sovereign Digital Identity solutions are built, where the data belongs to the user and he only shares with third parties those data essential to carry out a certain transaction. The data of each participant are trusted by the rest of the ecosystem because they are certified by trusted entities (financial institutions, public administrations, educational centers).

Finally, the programming capacity of the most advanced Blockchain platforms, with the so-called “Smart contracts”, allows “tokenizing” (representing digitally through a token or digital entity) real assets such as real estate, shares or works of art. Once digitized, these goods can be exchanged for other goods or for money, creating the “Internet of Value.” This ability makes it possible, among other things, to create “programmable money”, that is, to be able to send money to someone to be used for a certain purpose.

In our 2014 publication, “The Future of Money,” our experts analyzed the Phenomenon of Bitcoin, and already told us: “Bitcoin is a fundamental discovery of computing and a new and revolutionary tool to exchange money, property and, most basically, trust through the internet.” Since then, and fulfilling the forecasts of our experts, we have witnessed the emergence of thousands of cryptocurrencies and business solutions around them.

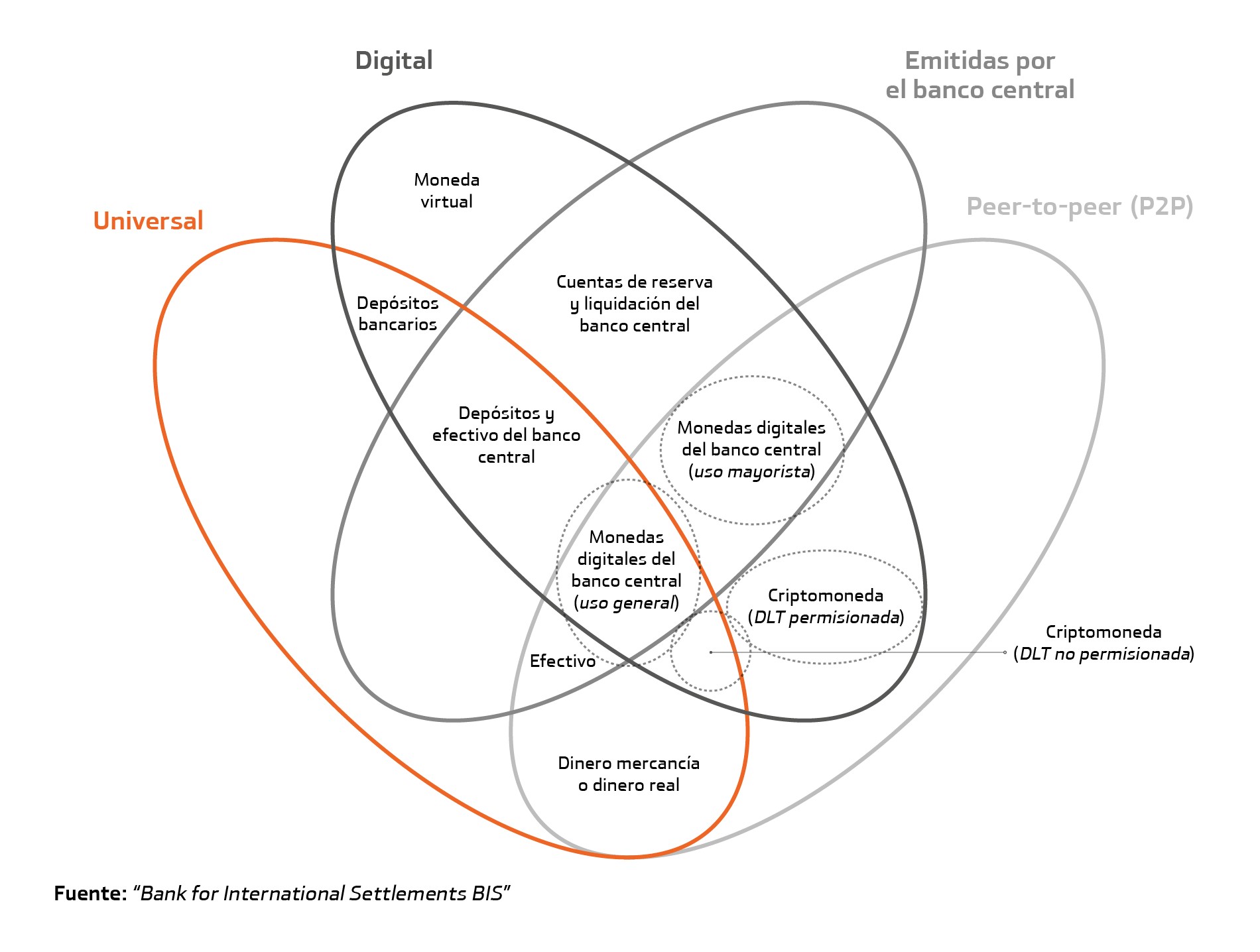

There is some confusion in the taxonomy of electronic money -being cryptocurrencies a type of electronic money-, so we start this section trying to clarify the concepts a little, relying on the recent work carried out by the BIS (Bank for International Settlements) and the IMF (International Monetary Fund).

We understand by money any asset that serves as a unit of account, store of value and means of payment. The illustration above serves to classify money and, within this classification, classify digital money (all that falls within the blue ellipse). For example, bitcoin would be a Cryptocurrency (permissive DLT).

Blockchain platforms are already a reality and are being applied in multiple areas. Cryptocurrencies are here to stay. Now, what is missing for its use to be massive and intensive?

How can you cross that chasm and reach widespread use? The answer is, as our FTF expert, Iker Marcaide, said, bringing real value to people: “Until all these innovations are stripped of the layer of complexity, he said, until we make them extremely simple for everyone to understand, they won’t become widespread.”

We believe that the keys to the future are threefold:

1. Regulators are open to innovation and even adopting it.

2. Simplification for the general public.

3. Standardization or, at least, interoperability between platforms.